Refinitiv: The European ETF industry enjoyed inflows over the course of May 2023. These inflows occurred in a further unstable market environment in which some asset classes showed positive results, while others performed negatively over the course of the month.

Sign up to our free newsletters

By Detlef Glow, Lipper’s head of EMEA research at Refinitiv

The market sentiment was still driven by hopes that central banks, especially the U.S. Federal Reserve, may have reached the last phase of their fight against the high and further increasing inflation rates and may, therefore, start to keep interest rates at least stable quite soon. Some investors already expect that there might be room for decreasing interest rates later this year. Nevertheless, there are still some concerns about geopolitical tensions, and the normalization of the disrupted delivery chains, as well as a still possible recession in the U.S. and other major economies around the globe. These fears are raised by inverted yield curves which are seen as an early indicator for a possible recession.

The performance of the underlying markets led in conjunction with the estimated net inflows to increasing assets under management (from €1,344.9 bn as of April 30, 2023, to €1,370.0 bn at the end of May). At a closer look, the increase in assets under management of €25.1 bn for May was driven by the performance of the underlying markets (+€17.3 bn), while the estimated net inflows contributed (+€7.7 bn) to the growth in assets under management.

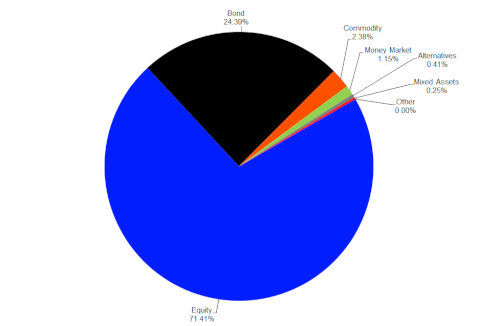

As for the overall structure of the European ETF industry, it was not surprising equity funds (€978.3 bn) held the majority of assets, followed by bond funds (€334.2 bn), commodities products (€32.7 bn), money market products (€15.7 bn), alternative UCITS products (€5.6 bn), mixed-assets funds (€3.5 bn), and “other” funds (€0.1 bn).

Graph 1: Market Share, Assets Under Management in the European ETF Segment by Asset Type, May 31, 2023

Source: LSEG Lipper

Fund Flows by Asset Type

The European ETF industry enjoyed estimated net inflows (+€7.7 bn). These flows were way above the rolling 12-month average (€6.9 bn).

The inflows in the European ETF industry for May were driven by bond ETFs (+€4.3 bn), followed by equity ETFs (+€2.7 bn), money market ETFs (+€0.8 bn), and mixed assets ETFs (+€0.1 bn). On the other side of the table, alternative UCITS ETFs (-€0.002 bn), “other” ETFs (-€0.01 bn), and commodities ETFs (-€0.2 bn) faced outflows for May 2023.

Source: ETFWorld

Subscribe to Our Newsletter