According to the principles of classical intermarket analysis, the correlation between these two asset classes should more often be inverse.

This dynamic stems from the fact that gold has historically served as a safe-haven asset during periods of geo-economic and/or geopolitical tension, phases in which the S&P 500 is more likely to weaken or lose momentum. Furthermore, gold is less attractive during periods of high real interest rates, as it cannot provide a yield comparable to that of bonds or high-yielding equities. In periods of high interest rates, the economy is more often growing and, consequently, the equity index is generally strong. In reality, things are more complicated and other parameters should be assessed.

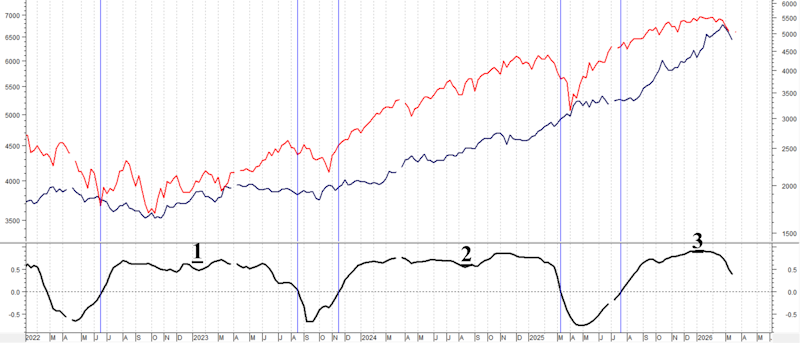

We will focus primarily on the relationship between the price of gold and the performance of the S&P 500 from the start of 2022 (weekly data):

The black line represents the return on the price of gold (right-hand logarithmic scale), the red line represents the value of the S&P 500 Index (left-hand logarithmic scale). At the bottom is the correlation between the two charts, calculated over 26 data points (i.e. 6 months of data). As can be seen, this correlation has been positive more often since June 2023.

I have highlighted three distinct phases in which there were periods of positive correlation:

- Between June 2022 and August 2023; during which both markets first fell and then rose, with the S&P 500 rising more sharply;

- From November 2023 to March 2025, with both markets rising, most notably for gold;

- From July 2025 to the present, where both markets have risen, but have been in a correction since late February and the correlation is declining.

The reasons for this persistent positive correlation between the two markets lie in the perception of gold as an asset class to hold in portfolios, not only during periods of tension, but above all as a hedge against the excess liquidity that the economic and financial system has been experiencing since 2020.

Gold’s current correction is also linked to the very sharp rise seen from August 2025 onwards. With the current phase of international tension, some institutional investors have had to liquidate positions quickly, and they usually start with those yielding the highest profits. Furthermore, there are widespread fears of rising inflation, and above all rising interest rates, which historically have a negative impact on the price of gold. We should also note that the dollar has strengthened during this crisis, making it less attractive for those holding currencies other than the dollar to buy gold.

Looking ahead, gold could find support, say, between $4,500 and $4,300. It could then gradually regain strength. The S&P 500 could also find support if tensions in the Middle East do not escalate. In this regard, the positive correlation could start to strengthen again in the coming months as both markets regain some strength.